O setor marítimo, responsável por aproximadamente 2,9% das emissões globais de carbono, busca atingir metas climáticas mais amplas, como o Acordo de Paris e o ‘Fit for 55’ na Europa. Uma vez que são os maiores navios, como os cargueiros, que tendem a contribuir mais para as emissões marítimas, isso representa um enorme desafio.

A IDTechEx vê os combustíveis verdes, como hidrogénio verde e ammonia, como algumas das soluções mais promissoras, com o novo relatório IDTechEx ” Fuel Cell Boats & Ships 2023-2033: PEMFC, SOFC, Hydrogen, Ammonia, LNG ” prevendo que o hidrogénio verde PEMFC (Proton-exchange membrane fuel cells) e os mercados SOFC de LNG/ammonia verde (célula de combustível de óxido sólido) crescerão rapidamente a 35% CAGR em um período de dez anos.

A IDTechEx vê os combustíveis verdes, como hidrogénio verde e ammonia, como algumas das soluções mais promissoras, com o novo relatório IDTechEx ” Fuel Cell Boats & Ships 2023-2033: PEMFC, SOFC, Hydrogen, Ammonia, LNG ” prevendo que o hidrogénio verde PEMFC (Proton-exchange membrane fuel cells) e os mercados SOFC de LNG/ammonia verde (célula de combustível de óxido sólido) crescerão rapidamente a 35% CAGR em um período de dez anos.

Why Hydrogen Fuel Cell Adoption Is Accelerating in Marine Markets, Explains IDTechEx

Author Luke Gear, Senior Technology Analyst

The maritime sector, which accounts for approximately 2.9% of global carbon emissions, is seeking to meet broader climate goals such as the Paris Agreement and ‘Fit for 55’ in Europe. Since it is the largest vessels, such as sea-going cargo vessels, which tend to contribute the most to maritime emissions, this presents a huge challenge.

IDTechEx sees green fuels, such as green hydrogen and ammonia, as some of the most promising solutions, with the new IDTechEx report “Fuel Cell Boats & Ships 2023-2033: PEMFC, SOFC, Hydrogen, Ammonia, LNG” predicting that green hydrogen PEMFC (proton exchange membrane fuel cell) and LNG/green ammonia SOFC (solid-oxide fuel cell) markets will grow rapidly at 35% CAGR over a ten-year period.

Today, liquified natural gas (LNG) vessels are the largest alternative fuel in marine markets. The global LNG fleet has been growing for decades, driven by an initial policy aimed at reducing localized emissions such as sulfur oxides, nitrous oxides, and particulate matter. However, the focus is now shifting towards reducing emissions of greenhouse gases, such as carbon dioxide and methane.

Indeed, new IMO (International Maritime Organization) policy includes an ‘Energy Efficiency Existing Ship Index (EEXI)’ and the Carbon Intensity Indicator (CII). EEXI ensures a ship is taking technical steps, in terms of how it is equipped and retrofitted, to reduce greenhouse gas emissions. CII is a measure of the carbon emissions per amount of cargo carried per mile and targets reducing emissions operationally. The measures are expected to become mandatory from 2023, with the first ship ratings given in 2024. Such regulations will be difficult to achieve without fundamental changes to the ways in which vessels are powered.

The new regulations undermine LNG use as a long-term solution because of methane slip, which occurs at every step in LNG’s lifecycle, alongside energy-intensive cooling (–161C) and re-gassing requirements. However, IDTechEx expects the regulations will create opportunities for alternative fuels, including green hydrogen, green ammonia, or e-fuels combined with carbon capture. To learn more about carbon capture and utilization, see the IDTechEx report “Carbon Dioxide (CO₂) Utilization 2022-2042: Technologies, Market Forecasts, and Players”.

The chemical energy held in alternative fuels can be converted into mechanical energy in multiple ways, including combustion; however, fuel cells offer great potential as a highly efficient solution, with a pathway to zero-emissions using green fuels. Currently, there are two main options for fuel cells in the marine environment – PEMFC, using green hydrogen, and SOFC, which are fuel flexible but notably can run on green ammonia, a derivative of green hydrogen.

Today, PEMFCs are the most technologically mature fuel cell technology. This has been driven by their high-power density and ambient temperature operation, making them suitable across various transport applications. Indeed, companies like Toyota, Hyundai, and Ballard have invested heavily in advancing and commercializing the technology in road sectors. While fuel cell vehicles have yet to demonstrate meaningful market adoption, the technological advancements behind them are enabling rapid commercialization in the marine sector.

Leading marine PEMFC suppliers include Nedstack, Powercell, and Ballard, which are vertically integrated pure-play companies. Corvus Energy is another notable contender with plans to release its first FC product over the next few years using fuel cells sourced from Toyota. While none of these companies began supplying fuel cells to the marine sector – Nedstack began with stationary power, PowerCell is a spin-out from Volvo, Ballard supplies heavy-duty road vehicles, and Corvus Energy is the leading maritime battery supplier – all have begun to pivot to the sector as opportunities have been created by regulation and funding.

Innovations from these players are also driving sales, with recent products greatly increasing power density and safety. Indeed, improvements include the use of novel stainless steel plate materials (increasing volumetric power density by around 40%) alongside double-walled hydrogen pipes, ventilation fans, and hydrogen sensors, allowing the fuel cell to be installed within the ship (rather than on the open-deck) – a gamechanger.

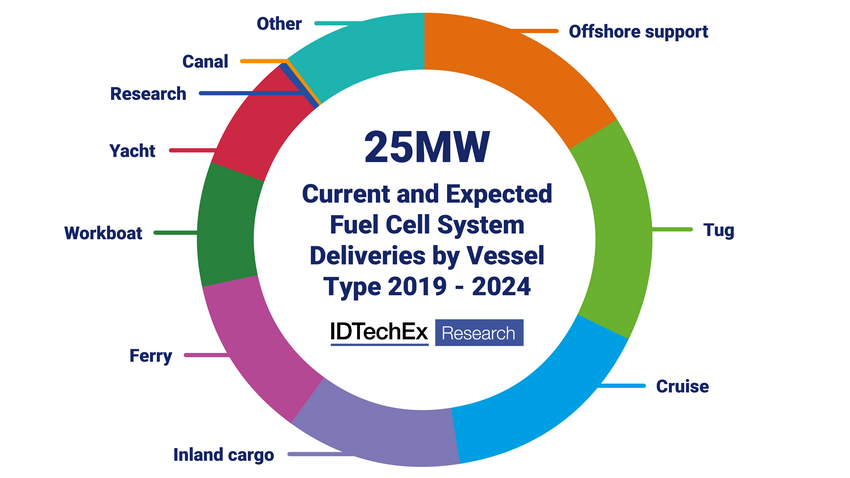

As is evident, the stars have been aligning for marine fuel cell markets over the past couple of years, and the average system size per vessel has now jumped to over 1MW, according to the project database tracked by IDTechEx in “Fuel Cell Boats & Ships 2023-2033: PEMFC, SOFC, Hydrogen, Ammonia, LNG”. Currently, end-use is dominated by a few large systems in inland cargo vessels, workboats, offshore support vessels (OSVs), tugs, cruise ships, and ferries. Amongst the largest orders are a 3.2MW PEMFC system from PowerCell, a 2MW SOFC system from Alma Clean Power (for the Viking Energy OSV), and individual 2MW PEMFC orders for the H-Tug and Ulstein OSV to be delivered by Nedstack.

Current and expected fuel cell system deliveries by vessel type 2019-2024. Source: IDTechEx in

Current and expected fuel cell system deliveries by vessel type 2019-2024. Source: IDTechEx in “Fuel Cell Boats & Ships 2023-2033: PEMFC, SOFC, Hydrogen, Ammonia, LNG”

IDTechEx expects that most orders in the mid-term will use PEMFC technology and remain in inland and coastal sectors (due to the volumetric limits of hydrogen). Nevertheless, the market today is just getting started, and the IDTechEx report predicts a total of 6MW will have been delivered to vessels by the end of 2022. Since most deliveries are pilot projects for fleet operators, each with fleet sizes of hundreds to thousands of similar vessels, repeat orders are poised to drive rapid market growth.

IDTechEx Research

This article is based on IDTechEx’s broad research portfolio, which tracks the adoption of electric vehicle demand & technology trends across land, sea, and air, helping you navigate whatever may be ahead. Find out more at www.IDTechEx.com/Research/EV.